7 Human Capital Risks Every Canadian Acquirer Must Test Before Close

Share

Badr Ait Ahmed

March 2, 2026

You’re about to commit capital to acquire a Canadian business. The price is set. The model assumes the founder transitions, key people stay, the operating culture integrates, and synergies materialize on schedule.

If any of those assumptions fail, you don’t get a partial outcome. You get a repriced deal, extended earn-outs, and 12–24 months of value erosion that no financial adjustment can recover.

The assumptions are the risk. And almost nobody tests them before signing.

Three hundred billion dollars in Canadian business revenues will change hands over the next five years. With 61% of SME owners now over 50 and 19% planning to exit within five years, Canada is entering its largest intergenerational wealth transfer in history.

The opportunity is real. BDC’s 2026 study shows acquirers who execute well see 4× profit uplift by year five. The market favours buyers — 10 potential acquirers for every 7 sellers.

But only 5% of first-time buyers take any preparatory steps before acquiring. Experienced buyers? Just 19%. EY’s research on M&A human capital gaps found that the people-related value destruction in acquisitions typically accounts for 10–15% of the total purchase price. That isn’t tail risk. It’s the median outcome when human capital assumptions go untested before close.

Here are the seven risks most Canadian acquirers never assess before close.

1. Leadership Continuity Risk

The deal assumption: The founder transitions smoothly, and the business continues to run.

In owner-operated businesses — the vast majority of Canadian SMEs — the founder often *is* the business. They hold client relationships, make key decisions, and embody the operating logic. When they leave faster than planned, the enterprise doesn’t just lose a person. It loses its decision-making system.

The BDC data confirms the exposure: 61% of SMEs are led by owners 50 or older. These transitions are retirement-driven and inevitable. PE practitioners have learned this the hard way — 58% of PE-backed CEOs are replaced within two years of acquisition (AlixPartners/Heidrick). In Canadian SMEs, where the founder and the CEO are often the same person, that replacement clock starts running at signing.

Before close, ask: Who truly runs the business day-to-day? What decisions can’t happen without the founder? What’s the realistic transition timeline — and what breaks if it compresses?

2. Key Person Revenue Concentration

The deal assumption: Revenue is an asset of the business, not of specific individuals.

Key employees carry client relationships, process knowledge, and institutional history that rarely exists in documentation. When they leave post-close — from uncertainty, misalignment, or competing offers — that revenue walks out permanently.

EY’s research quantifies the timeline: 47% of key employees leave within the first year post-acquisition, and 75% are gone within three years. First-year departure rates run 34% versus a 12% baseline in stable organizations — nearly 3× the normal rate (MIT Sloan). And replacing the people who leave isn’t simply a recruiting cost. The Center for American Progress found that replacing an executive can cost up to 213% of their annual salary, once institutional knowledge loss, productivity drag, and client relationship disruption are priced in.

Before closing, ask: Which roles are tied to specific revenue streams? What critical knowledge is undocumented? What retention mechanisms exist — and at what cost?

3. Cultural Execution Compatibility

The deal assumption: The two organizations will work together effectively after the close.

Culture isn’t values posters. It’s how decisions get made, how conflict gets resolved, and how work actually happens. When two organizations with incompatible operating cultures merge, friction shows up everywhere: slower decisions, passive resistance, and voluntary departures of the people you most need to keep.

Aon Canada’s 2023 M&A survey found that 59% of Canadian dealmakers say operating culture differences directly hindered value creation in their most recent deal, not a global average applied to Canada, but Canadian acquirers reporting their own outcomes. The BDC study confirms the timeline consequence: integration takes 12–24 months longer than expected. Mercer’s research found that 30% of deals that missed their financial targets cite culture misalignment as the root cause. Not market conditions. Not strategy failures. Incompatible operating systems were discovered after the price was locked.

Before close, ask: How are decisions made here versus in your organization? What behaviours get rewarded, and what gets punished? What happens when the two decision-making systems collide?

4. Operating Model Capacity

The deal assumption: The target’s operations can absorb growth or integration pressure.

98% of Canadian businesses have fewer than 100 employees. Small scale means informal processes, limited management depth, and founder-dependent operations. These work at the current size but break under growth pressure or integration load.

Acquirers planning to scale the target — or fold it into a larger operation — must assess whether the operating model can handle the transition. Role clarity, management capability beyond the founders, and process maturity determine whether scale creates leverage or chaos.

Before close, ask: Are roles clearly defined beyond the founder? Is there management depth at the second tier? Can current processes handle 2× volume without doubling headcount?

5. Synergy Execution Risk

The deal assumption: Synergies in the model will materialize on schedule.

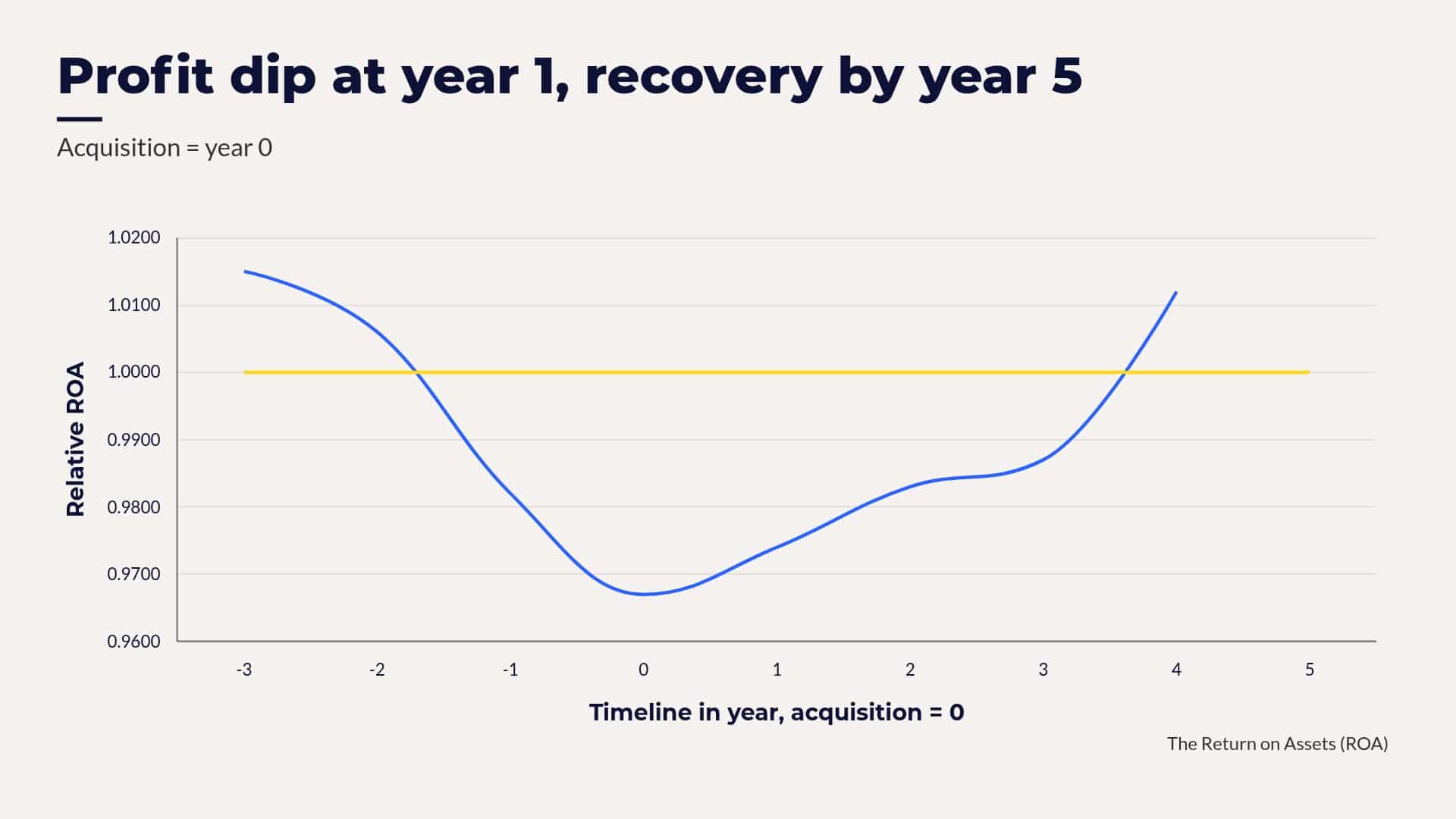

Every acquisition model includes synergy assumptions, cost savings, revenue acceleration, and operational efficiency. But synergies don’t happen automatically. They require deliberate planning, clear ownership, and execution capacity. The BDC data shows 4× profit uplift at year five, but also a short-term performance dip that’s normal. Acquirers who panic at the dip or who never planned for synergy execution abandon initiatives that would have delivered returns.

Aon Hewitt’s integration research found that 80% of failed integrations are characterized by significant productivity loss, the kind that erodes the very synergies the deal was built to capture. In Canadian SMEs, where the BDC data documents a 12–24 month integration delay as normal, every quarter of productivity drag is a quarter subtracted from your value creation window.

Before close, ask: Which specific roles drive synergy realization? Who owns execution on day one? What’s the 100-day plan, and what happens when it takes 200?

6. Integration Capacity Risk

The deal assumption: Leadership has the bandwidth to run the business and manage integration simultaneously.

Integration is a second full-time job. Someone has to run the existing business while someone else manages the merger. When the same people do both, something breaks, usually the core business that’s funding everything.

The BDC study found that core teams were consistently pulled away from operations during integration, and the workload was underestimated in nearly every case. Deloitte’s integration research puts the cost in concrete terms: integration alone runs 5–15% of deal value, and when combined with capability erosion and value leakage, the combined drag reaches 10–30% of deal value. In Canadian SMEs, integration management typically falls on the same two or three people running day-to-day operations. Something breaks.

Before close, ask: Who will run integration full-time? What current responsibilities will they drop? What happens if integration takes twice as long as planned?

7. Post-Close Value Preservation

The deal assumption: The asset retains its value after ownership changes.

Due diligence focuses on what’s wrong with the target. The bigger risk is what goes wrong after close. Key person departures spike. Clients leave with departing employees. Operating culture friction slows everything. The asset erodes before you capture its value.

The failure rate isn’t primarily about bad targets — it’s about unmeasured execution risk that was predictable before close. EY’s research on the human capital gap in M&A found that 75% of key employees leave within three years of an acquisition. The asset you underwrote and the asset you own 36 months later are not the same organization. The question is whether you modelled that gap before committing capital, or discovered it in the board report.

Before close, ask: What happens if 20% of key people leave in year one? What if the founder exits six months early? What’s the operating culture failure scenario — and how would you detect it before the P&L shows the damage?

The Preparation Gap

The numbers tell a clear story. $300 billion in Canadian deal value changing hands. 10–15% of the purchase price is consumed by the human capital gap (EY). 10–30% of deal value lost to integration friction and capability erosion (Deloitte). 5% of first-time buyers who take any preparatory steps before signing.

Capital isn’t the constraint. Deal flow isn’t the constraint. Execution readiness is.

The acquirers who capture the 4× upside are the ones who test the human assumptions behind the deal before committing capital, not the ones who discover the gaps 18 months after close.

What strategic decision are you making where the human impact hasn’t been modelled? [Start with a 60-minute diagnostic] — less than 1% of deal value to assess the risk that determines the other 99%.