Structured, data-driven human capital diligence does not replace the financial model. It completes it.

It maps the variables the model currently treats as constants: revenue concentration by key person and role, leadership depth against the operating model the acquirer intends to run, capability alignment between current skill distribution and thesis requirements, and organizational resilience, the actual capacity to absorb change without breakdown.

Each of these is measurable before close. Each has a financial translation: revenue at risk, EBITDA drag, integration timeline exposure, synergy capture probability.

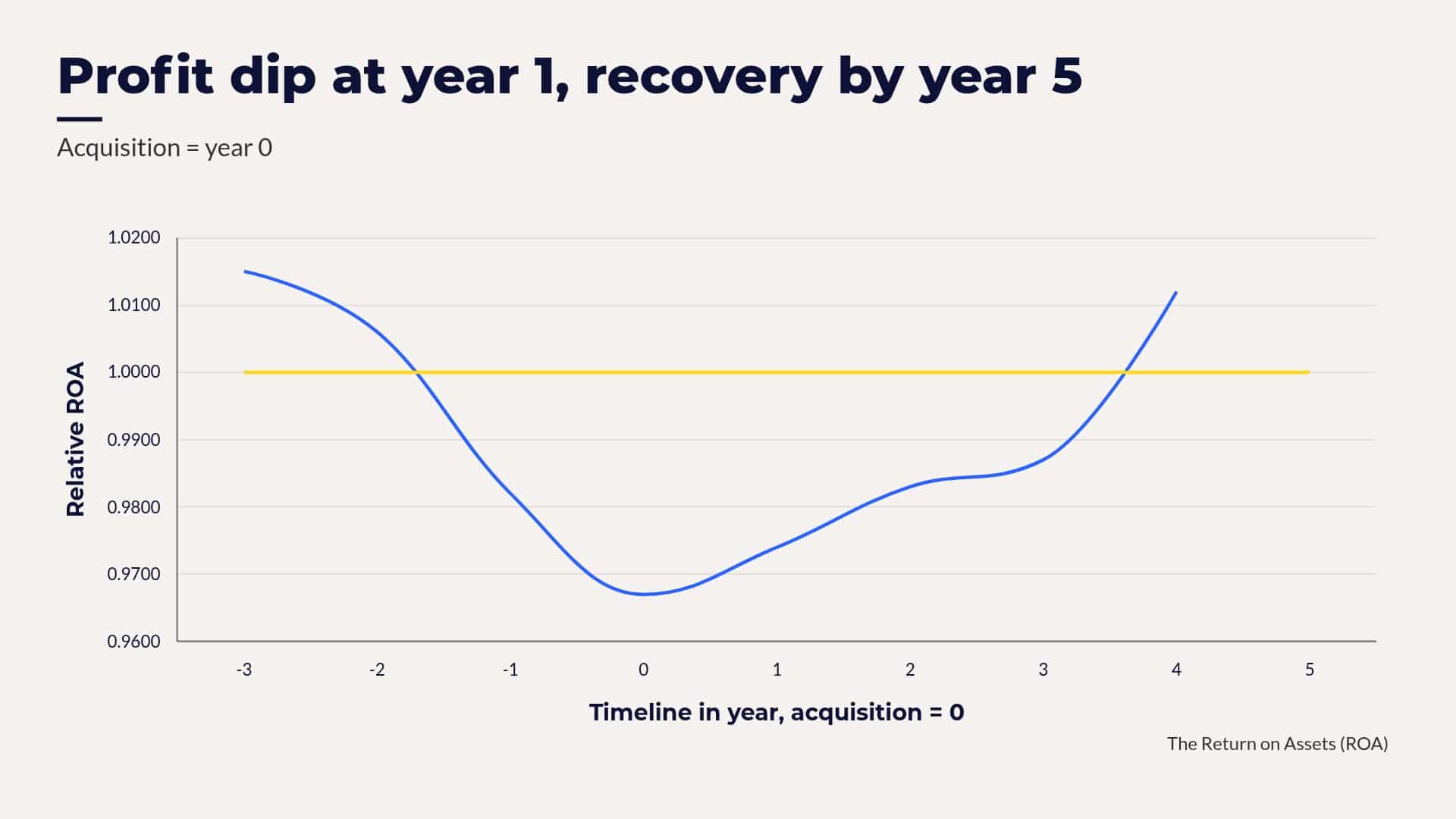

It also informs integration design, not just who to protect, but how aggressively to integrate. Research on post-acquisition integration finds that revenue synergy deals achieve the highest performance at intermediate integration levels. Over-integration disrupts the commercial structures and customer-facing relationships the thesis depends. The integration plan itself becomes a value-destruction mechanism when it is calibrated without knowing where the value actually sits and in which roles.

The cost of running a structured HC assessment before close is under one percent of deal value. The exposure it identifies typically runs five to twelve percent. The retention bonuses, integration consulting, and culture programs that substitute for it when risk surfaces post-close frequently exceed it, without recovering the value already lost.

Private equity and corporate development teams price legal risk, environmental risk, technology risk, and regulatory risk with structured frameworks. Human capital risk, the variable that determines whether the people who built the value will stay, perform, and execute under new ownership, is the last major line to run without one.

The data to build that framework has existed for years.

What strategic decision are you making where the human capital assumptions haven’t been tested?